Business Protection

When things don’t go according to plan,

what’s the bottom line for your business?

Find out more

Please note, for these insurance products, terms and conditions apply. This information is a summary only. You will receive a full policy document upon application. This policy will set out the terms, conditions and limitations of cover provided under the plan

Some of our latest reviews

We provide advice and recommendation

on the following areas of Business Protection

Have you considered what would happen to the shares of a shareholder, if something unexpected happened? If your business is critical to your income, your retirement and your family’s lifestyle, it makes sense to protect it. Shareholder Protection or Ownership Protection offers peace of mind for you, your business partners and the long term future of your business, while taking care of your family financially too.

Shareholder Protection is a vital tool to provide you with a lump sum in the event of death or critical illness and this would enable your company to buy the shares of the relevant business co-owner.

Without Shareholder Protection an unexpected event could be devastating for the business and its structure. If a co-owner or shareholder were to die, the shares could go into the deceased estate and commonly be inherited by the spouse (or partner). This may cause a number of serious problems, such as:

- Raising capital to acquire shares if the spouse or partner decides to sell.

- Ensuring the spouse or partner receives a fair price for the shares.

- Avoidance of the shares falling into the deceased state.

- The introduction of an unsuitable buyer of the shares.

- Unfavourable prospects of the spouse or partner keeping the shares.

- Any impact on the confidence and productivity of employees.

- Attraction from competitors and the poaching of key staff.

We understand how hard our clients work to build their businesses, making many sacrifices along the way to create regular income, build an asset and provide for their family. In that context, we strongly believe that not having Shareholder Protection is a false economy.

The real question is; can you afford not to have it?

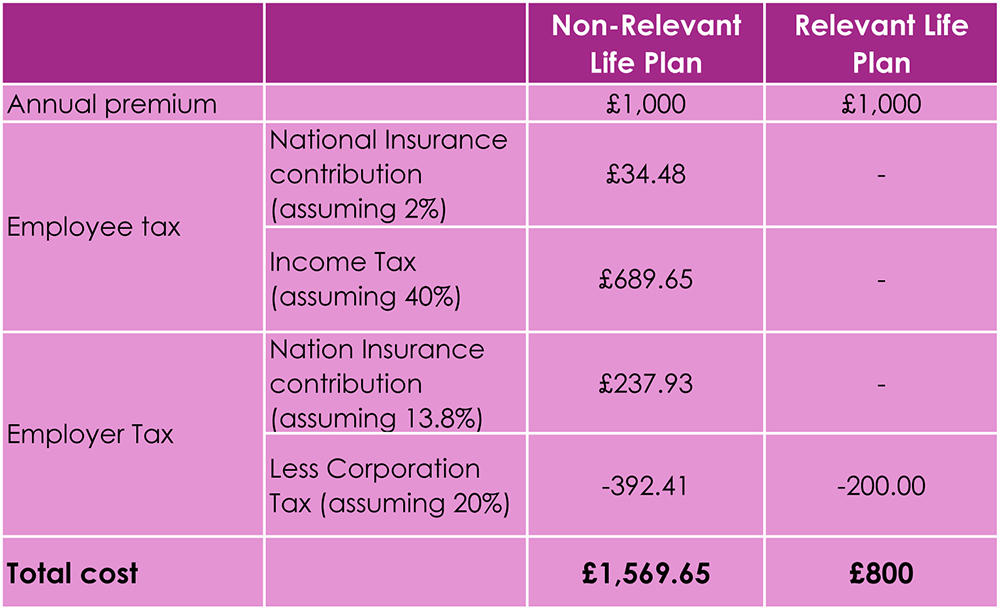

Providing added peace of mind for your people is a benefit to both them and your business. As part of a wider benefits package, a tax efficient Relevant Life Plan (RLP) can help to attract and retain the best people. Which in turn will help your business to thrive and grow.

RLP offer life cover that is highly tax efficient – in fact, we can show you how this type of policy may be able to save up to 50% on the cost of a conventional life policy.

A RLP is a simple term assurance product popular among owners of Limited Companies. We listen to your circumstances and advise on a suitable policy to meet your needs. Set up and paid for by the employer, the Plan will pay out a tax-free lump sum (under legislation current in tax year 2015/16) to the employee’s loved ones, should they pass away during the term of the policy.

RLPs make it possible for employers with just a few employees, high earners and Directors to take advantage of ‘death in service’ benefits.

If all qualifying conditions are met and your accountant is aware of the tax consequences of the RLP, then the arrangement can save over 40% if the life assured is a basic rate tax payer, or almost 50% if the life assured is a higher rate tax payer (under legislation current in tax year 2015/16).

We can work directly with your Accountant, answering their queries and ensuring you benefit from the tax savings.

Comparing the cost of a Non-Relevant Life Insurace policy to a Relevant Life Plan

In our experience, we have often seen Company Directors who are paying too much for their personal life assurance from their personal finances.

A RLP will help ensure you are covered, without compromise, in a tax efficient manner. We’re happy to discuss the excellent savings that may be possible with your Accountant and advisors from the outset.

Unfortunately, sole traders, equity partners of a partnership or equity members of a Limited Liability Partnership cannot take advantage of RLPs. If that’s you, ask us what your best alternatives are.